Introduction

In Part 1, I introduced the Clarity Gap in cyber underwriting.

The problem is not missing data. It is unstable interpretation.

In Part 2, I get specific about what closing that gap actually looks like — and why Astragar was purpose-built to operationalise it:

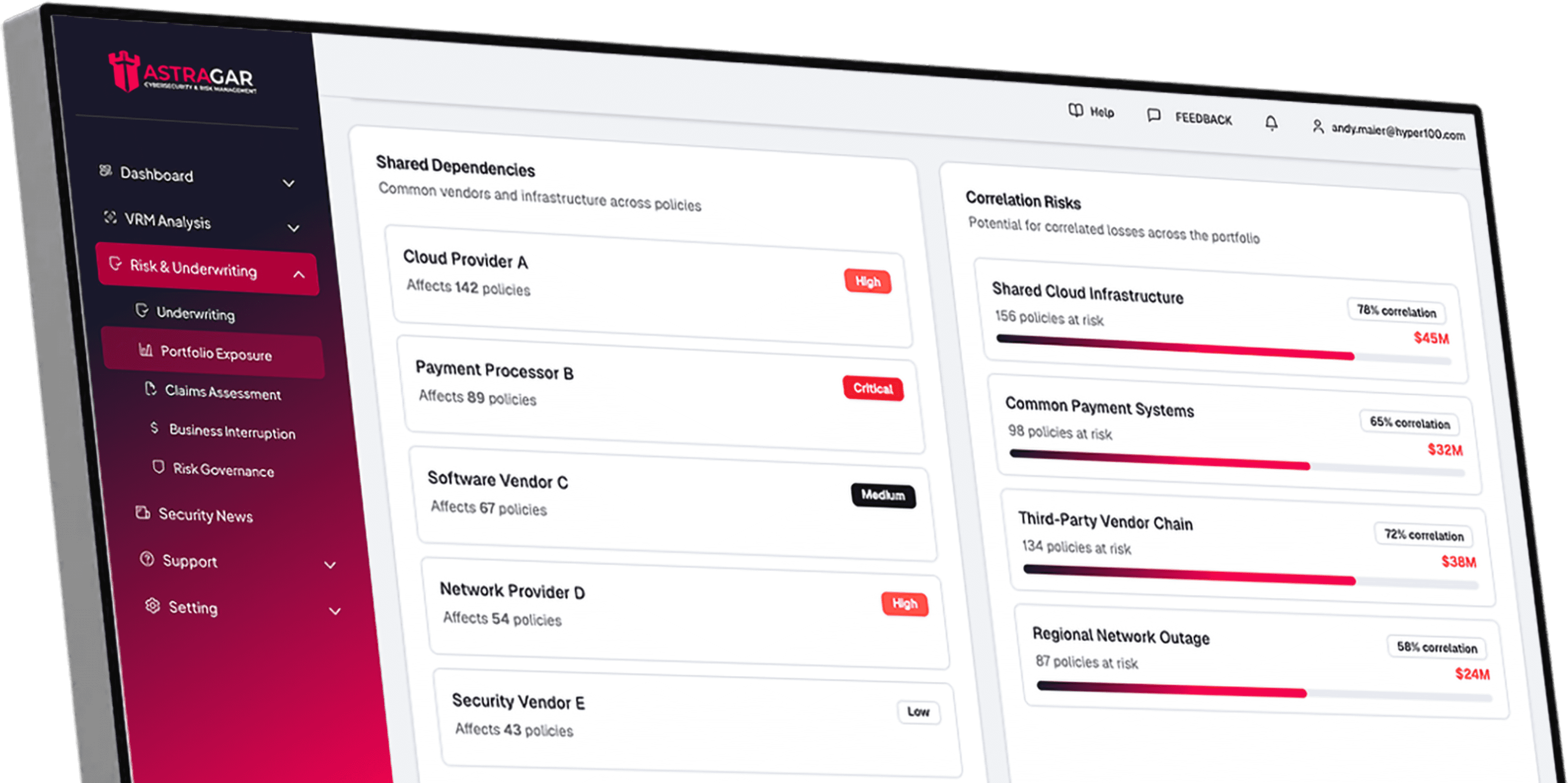

• Map vulnerabilities to the business systems that actually matter for insured exposure

• Add exploit context — in practice, only 20–30% of scan findings typically merit serious underwriting attention

• Translate exposure into probable loss scenarios before pricing decisions are made

When that translation becomes structured, underwriting decisions become more consistent, more defensible, and far less prone to late-cycle repricing.

Part 3 coming next: what happens to portfolio-level exposure when you apply this framework at scale.

Part 2 of the Clarity Gap Series

Cyber insurance underwriting does not struggle because data is missing. It struggles because interpretation is inconsistent.

In Part 1, I introduced the Clarity Gap: the distance between technical security findings and the defensible pricing decisions insurers must ultimately make.

In this piece, I want to get specific about what closing that gap actually looks like inside an underwriting cycle — and why it matters enough that Astragar was purpose-built to operationalise it.

Cyber underwriting increasingly draws on multiple technical inputs — including vulnerability scans, external attack surface monitoring, threat intelligence feeds, and internal security assessments.

The volume of available security data has grown dramatically over the past decade.

What has not kept pace is the ability to translate that data into consistent, defensible decisions.

That gap between data and decision is where pricing discipline breaks down.

The Translation Problem

Most insured organisations already run vulnerability management programmes and produce large volumes of technical security data. The challenge is not detection. The challenge is translation.

Before pricing cyber risk, underwriting teams must reliably answer three questions:

1. Which vulnerabilities affect systems that directly support insured business services?

2. Are those vulnerabilities realistically exploitable in the current threat environment?

3. If exploited, what is the probable financial impact?

Without a structured approach to those three questions, underwriting teams cycle back through the same datasets repeatedly. Risk engineers are re-engaged to reassess exposure. Reinsurers request additional clarification. Pricing adjustments happen late in the process. In practice, the same raw vulnerability data produces different underwriting conclusions depending on who is reviewing it and when.

The issue is not a lack of data. It is unstable interpretation.

The Three-Step Fix Astragar Was Built to Deliver

Astragar was developed in direct partnership with one of the world’s five largest insurance brokers, specifically to close this interpretation gap inside live underwriting workflows. The framework has three steps.

Step 1: Map Vulnerabilities to Business Systems

Not every vulnerability meaningfully affects insured exposure. Findings that intersect with externally exposed systems supporting core business services represent fundamentally different risk conditions than vulnerabilities buried in internal environments. Underwriting discipline begins by identifying where vulnerabilities actually intersect with operational continuity. In our experience, this mapping step immediately removes the majority of raw findings from the pricing conversation.

Step 2: Introduce Exploit Context

Technical severity scores do not reflect attacker behaviour. A CVSS 9.8 vulnerability on a system with no internet exposure is a different risk than a CVSS 6.5 vulnerability actively targeted by ransomware tooling.

When exploit intelligence, observed attacker activity, and threat tooling data are layered in, the set of vulnerabilities that meaningfully influence underwriting decisions typically contracts to 20–30% of the original scan output. That is the subset that should be driving pricing. The rest is noise.

Step 3: Translate Exposure into Probable Loss Scenarios

Once vulnerabilities are mapped to business systems and filtered through exploit context, underwriting teams can evaluate probable operational disruption and financial impact. At this stage, pricing decisions are grounded in exposure conditions rather than raw vulnerability volume.

The objective is not certainty. The objective is stable decision logic — conclusions that hold up when risk engineers, reinsurers, and senior underwriters review the same file.

Why This Improves Underwriting Discipline

When vulnerability signals are interpreted through a consistent structured framework, underwriting outcomes become more predictable and portfolio exposure becomes easier to manage. Fewer late-cycle pricing adjustments. Fewer reinsurer clarification cycles. Fewer re-engagements of risk engineering mid-process.

This approach does not eliminate cyber risk. It improves the quality of the decisions surrounding it — and in a market where pricing discipline is increasingly difficult to maintain, that difference is material.

Cyber insurance will continue to evolve as threat actors, technologies, and business dependencies change. Underwriting frameworks that reliably translate technical signals into defensible financial reasoning will remain the foundation of any sustainable book.

astragar.com/clarity-gap

See It Applied to Your Own Risk Profile

If you are seeking cyber insurance, preparing for renewal, or looking to strengthen how your organisation demonstrates cyber risk to insurers, we offer a focused 15-minute Clarity Gap call.

In that call, we will walk through the three-step framework using your organisation’s own risk profile as the working example — so you leave with a view of where the translation gap exists in your current process and what structured interpretation would change.

Whether you are:

a small or medium business — gain clearer visibility into the vulnerabilities most likely to affect insurability, resilience and premium outcomes

a mid-sized enterprise — improve prioritisation by linking technical findings more directly to business services, operational exposur, and probable loss scenarios

a large enterprise — bring greater consistency, defensibility and financial clarity to complex risk portfolios across multiple systems, teams, and business units

Book your 15-minute Clarity Gap call: https://meetings-eu1.hubspot.com/amitabh-roy/pilot

See your cyber risk in $ terms — not CVSS scores.