The cyber insurance market has experienced material volatility over the past several years. According to NAIC reporting, U.S. cyber direct written premiums reached approximately $9.1 billion in 2024, following multiple years of rate hardening and loss pressure. During peak ransomware cycles, standalone cyber loss ratios exceeded 65%, prompting significant underwriting recalibration.

Exposure complexity, however, has not been simplified.

The 2025 Verizon Data Breach Investigations Report analyzed more than 22,000 security incidents and over 12,000 confirmed breaches, with 44% involving ransomware. At the same time, enterprises routinely manage tens of thousands of vulnerabilities across distributed environments. Research consistently shows that fewer than 5% of disclosed vulnerabilities are ever actively exploited, and CISA’s Known Exploited Vulnerabilities catalog represents only a small fraction of total CVEs.

The structural issue is not data scarcity. It is a translation.

The Clarity Gap is the disconnect between security risk signals and defensible business decisions.

In cyber insurance underwriting, that disconnect appears when technical severity scoring becomes a proxy for pricing logic. Cyber risk is evolving from signal management to decision-grade intelligence, but underwriting frameworks have not fully made that transition.

Where CVSS Fails Pricing Logic

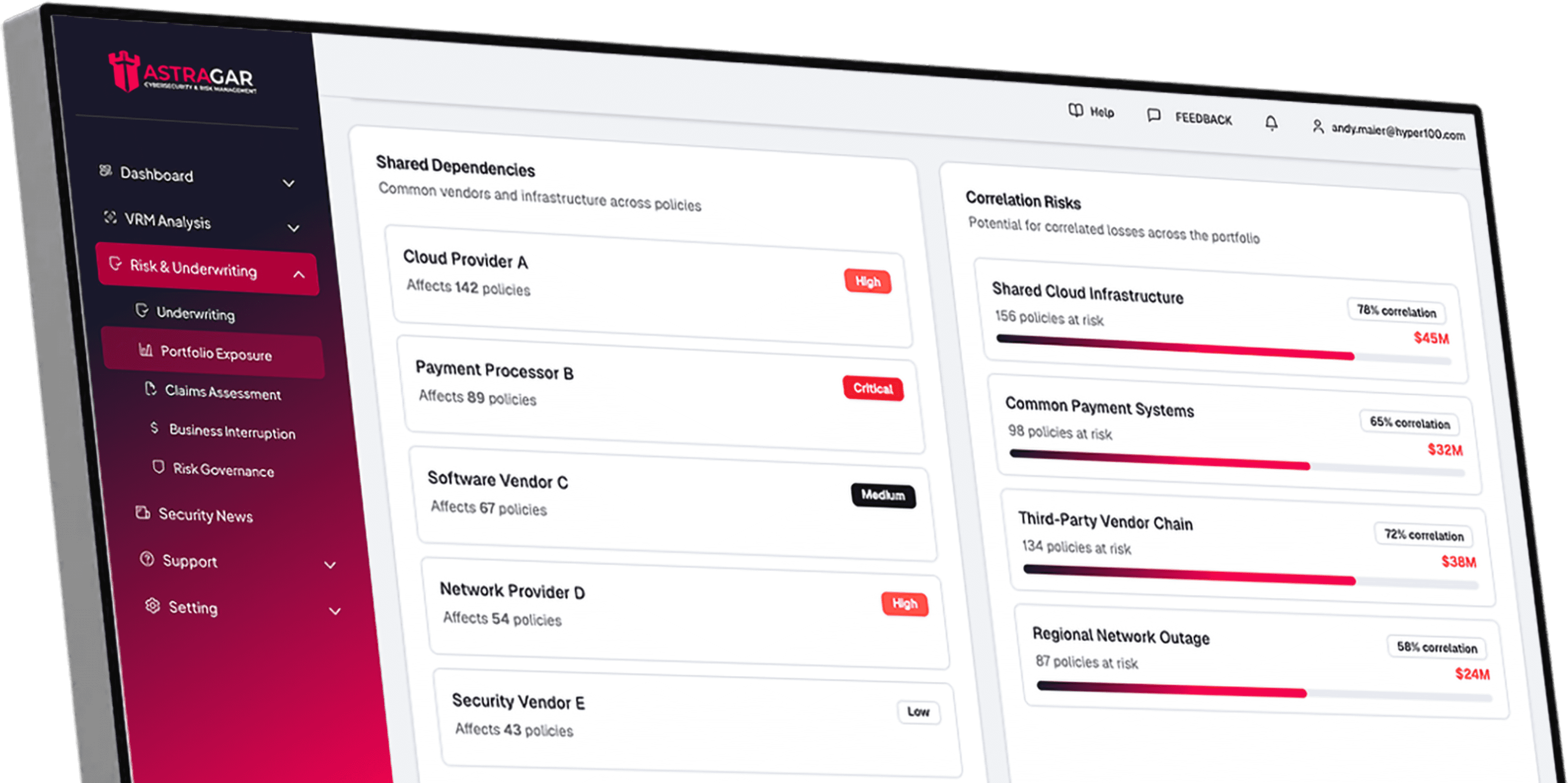

Cyber insurance submissions routinely include vulnerability scans. In many underwriting workflows, vulnerability severity (often derived from CVSS-based scanner outputs) is a key quantitative signal used to assess exposure and patch management effectiveness.

CVSS was designed to describe inherent technical severity. It was not designed to inform pricing decisions, attachment strategy, retention structure, or portfolio consistency.

Consider a submission reporting thousands of vulnerabilities across internal systems. Several carry high CVSS ratings but affect low-exposure infrastructure. Meanwhile, a moderately rated vulnerability impacts an externally facing authentication system tied directly to revenue and customer access.

From a scoring perspective, the higher rating appears more urgent. From an underwriting perspective, the externally exposed vulnerability may represent materially higher expected loss.

When severity scoring substitutes for exposure mapping, pricing decisions detach from financial consequence. That disconnect represents the first operational layer of the Clarity Gap.

Static Severity in a Dynamic Threat Environment

CVSS scores are static and context-neutral. Cyber threat activity is not.

Ransomware accounts for nearly half of confirmed breaches in recent reporting. Business email compromise losses exceeded $2.7 billion in 2024 alone, with more than $17 billion reported over the past decade in the United States.

Threat actors prioritize leverage and operational disruption, not theoretical severity ratings. When underwriting relies heavily on static scoring, two distortions emerge:

Conservative overpricing based on theoretical severity without credible exploit probability

Underestimation of vulnerabilities that are actively targeted but not rated at the highest level

Both outcomes reduce pricing consistency in a market where underwriting defensibility is increasingly scrutinized.

If two underwriters reviewing the same scan reach materially different conclusions, the inconsistency may reflect the interpretive framework rather than the underlying exposure.

Financial Consequence Defines Decisions

Underwriting ultimately turns on expected loss. Two systems may carry similar CVSS ratings. One supports peripheral internal functions. The other underpins core revenue processing. The rating may be similar. The exposure profile is not.

Without translating vulnerability data into probable financial impact, underwriting decisions default to generalized buffers or assumed resilience. In a market where 50–65% of global cyber premiums are ceded to reinsurance, capital providers demand greater clarity.

Reliance on CVSS as a primary underwriting signal introduces structural ambiguity.

That ambiguity is the Clarity Gap.

For those underwriting cyber risk today: how much weight do CVSS severity scores still carry in pricing decisions, and where do they meaningfully fall short?

See your cyber risk in $ terms — not CVSS scores.